- US: +1-408-610-2300

- Toll Free: +1-866-831-4085

- Become a Client

The global ultra-thin glass market size has generated a revenue of USD 14.17 billion in 2018. It is expected to witness growth with a 10.1% CAGR over forecasted years, 2019 to 2025. This can be associated with the surging usage of consumer electronic appliances like laptops, computers, and televisions. Further, the rising demand for flat panel displays across countries across the world is projected to drive market demand in upcoming years.

This glass is prominently used across the electronics industry on account of properties like corrosion and abrasion resistance, transparency, surface smoothness, and flexibility. Thus, such glasses find a wide range of applications in the production of semiconductors, display and touch panels, optical & electronic sensors, and organic electronic devices like moisture and oxygen barriers.

The increasing demand for LEDs, LCDs, OLEDs, laptops, monitors, and smartphones has paved the way for the usage of flat panel displays. For instance, in 2018, Xiaomi had launched a Smartphone named Hongmi Note 5 across South Korea that used ultra-thin tempered glass with 0.3 mm thickness. Thus, increasing usage of such smartphones coupled with surging display sizes is expected to drive the market in upcoming years.

The increasing demand for LEDs, LCDs, OLEDs, laptops, monitors, and smartphones has paved the way for the usage of flat panel displays. For instance, in 2018, Xiaomi had launched a Smartphone named Hongmi Note 5 across South Korea that used ultra-thin tempered glass with 0.3 mm thickness. Thus, increasing usage of such smartphones coupled with surging display sizes is expected to drive the market in upcoming years.

The segment of smartwatches is also gaining momentum across the wearable industry. Several prominent players like Fitbit, Apple, Garmin, and Samsung have sold around 5.5 million, 22.5 million, 3.2 million, and 5.3 million units respectively, in 2018. This increased smartwatch production is also expected to drive demand for ultra-thin glasses during forecasted years, 2019 to 2025.

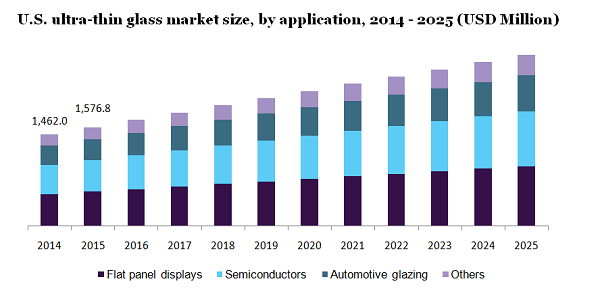

The ultra-thin glass market can be segmented based on applications such as semiconductors, automotive glazing, flat panel displays, and others. The flat-panel display held the largest share of around 38.3% across the global market in 2018. This can be associated with rising consumer electronics demand across the globe.

This glass is predominantly used in the manufacturing semiconductors for interposer applications and chip packaging due to its features of being transparent and operating on higher frequency thereby boosting the product efficiency. Further, the surging demand for such integrated chips for producing sensors, LED lightings and networking devices photovoltaic inverters, machine-human interface systems, and smart meters is projected to drive market growth in the upcoming years.

The automotive glazing segment is expected to register a 5.7% CAGR in upcoming years due to increasing lightweight car demand. Several benefits like good impact resistance and lightweight properties are anticipated to drive demand for the production of automotive windows. This weight reduction helps in lowering CO2 emissions and improving the fuel efficiency of the vehicles. These factors are anticipated to drive demand for such glasses across the automotive glazing segment.

The other segment includes organic electronics, solar panels, and energy storage devices. The growth for this segment can be associated with features like eco-friendly, good optical quality, improved scratch resistance, and energy-efficient features. Several players across this market are engaged in product innovation for boosting their usage across the emerging organic electronic sector. For example, a product named SPOOL was launched by AGC which is largely being used for the manufacturing of touch panels, organic LEDs, and flexible displays.

In 2018, Asia Pacific dominated the global ultra-thin glass market with a share of around 70.5% across the global market. This growth can be associated with surging demand for displays having flat panels across South Korea, India, and China. Nearly 50% of the global fabrication plants for flat panel displays are located in China.

Several companies producing the LEDs are willing to establish a strong base across these countries on account of increasing customer demands. For example, in 2018, Corning Incorporated has opened a manufacturing facility in Anhui province located in China for producing an LCD glass substrate. This facility manufactures Gen 10.5 substrates with TFT-grade by using named as EAGLE XG Slim glass.

In 2018, the U.S. dominated the North American market for ultra-thin glass due to the presence of a large industry of semiconductors. As stated by SIA (Semiconductor Industry Association), this country held a share of around 45% across the global market of semiconductors.

The 8-point plan created by SIA which included trade, research, workforce, tax, environment, export control, health and safety, intellectual property, and anti-counterfeiting helped the semiconductor industry to strengthen across the U.S. This initiative undertaken by SIA boosted market growth for semiconductors thereby fueling up demand for ultra-thin glass.

Europe is anticipated to witness a 6.4% CAGR during the forecasted period, 2019 to 2025. This growth can be associated with surging demand across LEDs, LCDs, automotive, and solar energy sectors. As stated by the SPE (Solar Power Europe), a reduction of about 40% in the emission of greenhouse gases was targeted by Europe. Thus, countries like Germany are striving to increase the solar capacity installation to 8GW for attaining this renewable target, thereby driving the demand for ultra-thin glasses.

The outbreak of the COVID-19 virus has negatively impacted the market for ultra-thin glass. The imposition of lockdown and trade restrictions have stagnated the industrial demand for ultra-thin glass. As the majority of the key manufacturers of ultra-thin glass are located in China, limitations in their supply chain across other countries have also adversely affected the market growth. But, the demand for LED displays in smartphones, laptops, and televisions has augmented due to work from home policies and the emerging concept of online education. Such factors are projected to drive the market growth for ultra-thin glass to some extent in the post-pandemic period.

Key players in the market are Corning Incorporated, AGC Inc., SCHOTT AG, Xinyi Glass, and Nippon Electric Glass. The strategy of capacity expansion is largely being followed by the players across this industry.

These players are engaged in product development and innovation to gain a competitive advantage over other players. For example, CSG Holding Co., Ltd. had announced the construction of a kiln for producing an ultra-white special and electronic glass having 0.33mm to 1.1mm thickness that can be used for producing protective tempered electronic glass, especially for smartphones.

|

Attribute |

Details |

|

The base year for estimation |

2018 |

|

Actual estimates/Historical data |

2014 - 2017 |

|

Forecast period |

2019 - 2025 |

|

Market representation |

Revenue in USD Million; Volume in Million Square Meters; CAGR from 2019 to 2024 |

|

Regional scope |

North America, Europe, Asia Pacific, Central & South America, Middle East & Africa |

|

Country Scope |

U.S., Germany, China, India, South Korea, and Brazil |

|

Report coverage |

Volume and revenue forecast, company share, competitive landscape, growth factors, and trends |

|

15% free customization scope (equivalent to 5 analyst working days) |

If you need specific information, which is not currently within the scope of the report, we will provide it to you as a part of the customization |

This report forecasts revenue growth at the global, regional, and country levels and provides an analysis of the latest industry trends from 2014 to 2025 in each of the sub-segments. For the purpose of this study, Million Insights has segmented the global ultra-thin glass market report based on application and region:

• Application Outlook (Revenue, USD Million; Volume, Million Square Meters; 2014 - 2025)

• Flat panel displays

• Semiconductors

• Automotive glazing

• Others

• Regional Outlook (Revenue, USD Million; Volume, Million Square Meters; 2014 - 2025)

• North America

• U.S.

• Europe

• Germany

• the Asia Pacific

• China

• India

• South Korea

• Central &South America

• Brazil

• Middle East & Africa (MEA)

Research Support Specialist, USA